Loan app subscription fees are worth it when you take at least two to four advances per month and you use the non-advance features (credit building, overdraft alerts, budgeting) enough to justify the fixed cost; they are not worth it when you borrow once in a while, forget to cancel, or treat the $8.99 monthly charge as free. On a single $100 advance repaid in seven days, Brigit's $8.99 membership attributes roughly 468% effective APR to that one transaction. Spread across four advances that same month, the per-advance cost collapses to the low double digits. The question is never "is the subscription cheap." The question is how many times you actually press the button.

Why Subscriptions Took Over the Category

Subscription pricing became the default model in 2025 and 2026 because it sidesteps federal disclosure rules. The CFPB's December 23, 2025 Advisory Opinion and the withdrawal of the July 2024 proposed interpretive rule left subscriptions outside the TILA finance-charge definition (the CFPB's Junk Fees initiative tracks the broader debate). That means the one cost almost every user pays is also the one cost no app is required to fold into its APR disclosure.

Empower rebranded to Tilt in August 2025, kept the $8 monthly fee, and kept the 0% APR language on its advances. Dave transitioned in February 2025 from a tip model to a 5% flat advance fee sitting alongside a $1 to $15 monthly subscription. Brigit held at $9.99 for Plus and $14.99 for Premium. The common thread: monthly recurring revenue the user has to calculate themselves if they want to know the real cost of borrowing.

The Real Math: Break-Even per Advance

Here is the cost of one advance from a subscription app, generalized:

Per-advance cost = (monthly subscription / number of advances that month) + (expedite fee) + (any tip or flat advance fee).

Then annualize:

Effective APR = (per-advance cost / advance amount) x (365 / repayment days) x 100.

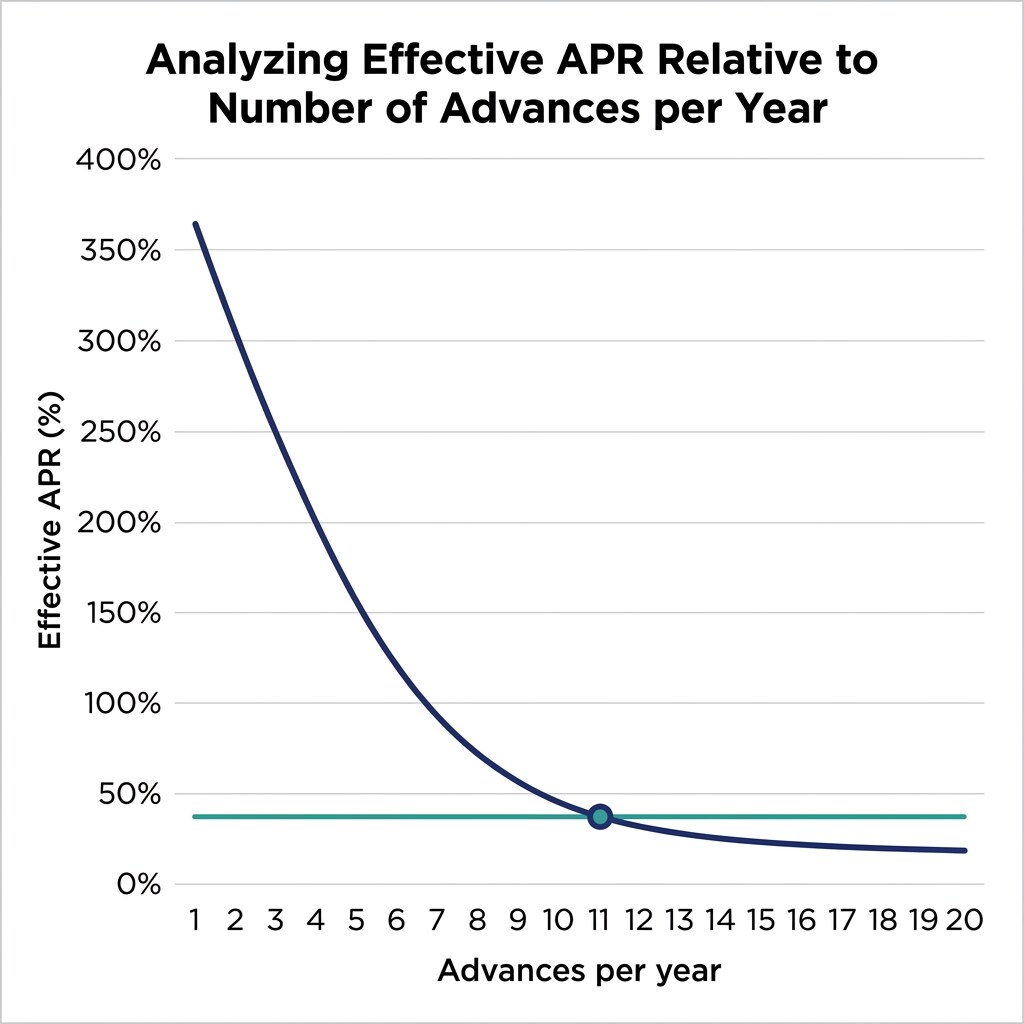

A Brigit Plus user who takes one $100 advance and repays in 7 days, fully attributing the $8.99 subscription to that advance: ($8.99 / $100) x (365 / 7) x 100 = 468.8% effective APR. Same user taking four $100 advances in the month, each 7-day, splits the sub four ways: ($2.25 / $100) x (365 / 7) x 100 = 117.4% per advance. Eight advances in a month: 58.7% per advance.

The subscription is not inherently expensive or cheap. It is a fixed cost that amortizes across usage. The more you borrow, the cheaper each borrow gets. Which is, on its own, a mildly unsettling incentive structure.

What Each Subscription Actually Buys You

The advance is only part of the bundle. Every app sells the subscription as access to a broader product. Whether that broader product is worth the fee is the second half of the worth-it question.

| App | Monthly Fee | Max Advance | What's Included Beyond the Advance |

|---|---|---|---|

| Brigit | $8.99 Plus / $14.99 Premium | $250 | Budgeting tools, credit builder, overdraft alerts, free Express delivery (Premium only) |

| Dave | $1 to $15 depending on tier | $500 | Checking account, credit building, ExtraCash advances, Dave Banking features |

| Empower / Tilt | $8 | $300 | Credit line $200 to $1,000, AutoSave, credit monitoring, 0% APR advances |

| MoneyLion Credit Builder Plus | $19.99 | Varies (Instacash boost) | Credit builder loan, investing account, Instacash limit increase |

| Klover | $0 (ad-supported) | Up to $200 | Points-unlocked advances, surveys and ads for higher limits |

Empower/Tilt has over 250,000 App Store reviews at 4.8 stars and 200,000+ Google Play reviews at 4.7 stars as of late 2025. That is not a casual user base. But review volume is not break-even math. A user who signs up for Tilt, takes one $200 advance a month, repays in 10 days, and never opens the credit monitoring module is paying $8 for a feature they use and effectively ignoring the rest.

When the Subscription Is Genuinely Worth It

- You borrow two or more times per month. The arithmetic starts working in your favor around the third advance.

- You actually use the credit-builder product. MoneyLion Credit Builder Plus at $19.99 is expensive, but a user who makes 12 months of on-time payments and builds a 30 to 60 point FICO lift is getting something the advance alone does not deliver.

- You prefer a fixed cost to a variable tip. Brigit has no tips. For borrowers who found tip-model apps psychologically coercive, the flat fee is the product.

- Your alternative is a $35 overdraft fee. One avoided overdraft per month pays for every subscription on this list.

When It Isn't

- One-time borrowers. If you advanced $150 last March and the app has been charging you $8.99 every month since, you have paid $107.88 for one $150 transaction. That is 71.9% of the loan in pure subscription cost.

- Low-balance, set-and-forget accounts. The most common complaint pattern across App Store reviews and Trustpilot is "I forgot I was still paying." Brigit drew an FTC action in November 2023 over disputed practices around cancellation clarity. Brigit settled; the company disputed the FTC's characterizations. The underlying friction (forgotten subscriptions) is real across the category.

- Users who only want the advance. Klover is free, ad-supported, and caps at $200. For a once-in-a-while $100 borrower, free-with-ads is almost always cheaper than $8.99 a month.

The Cancellation Question

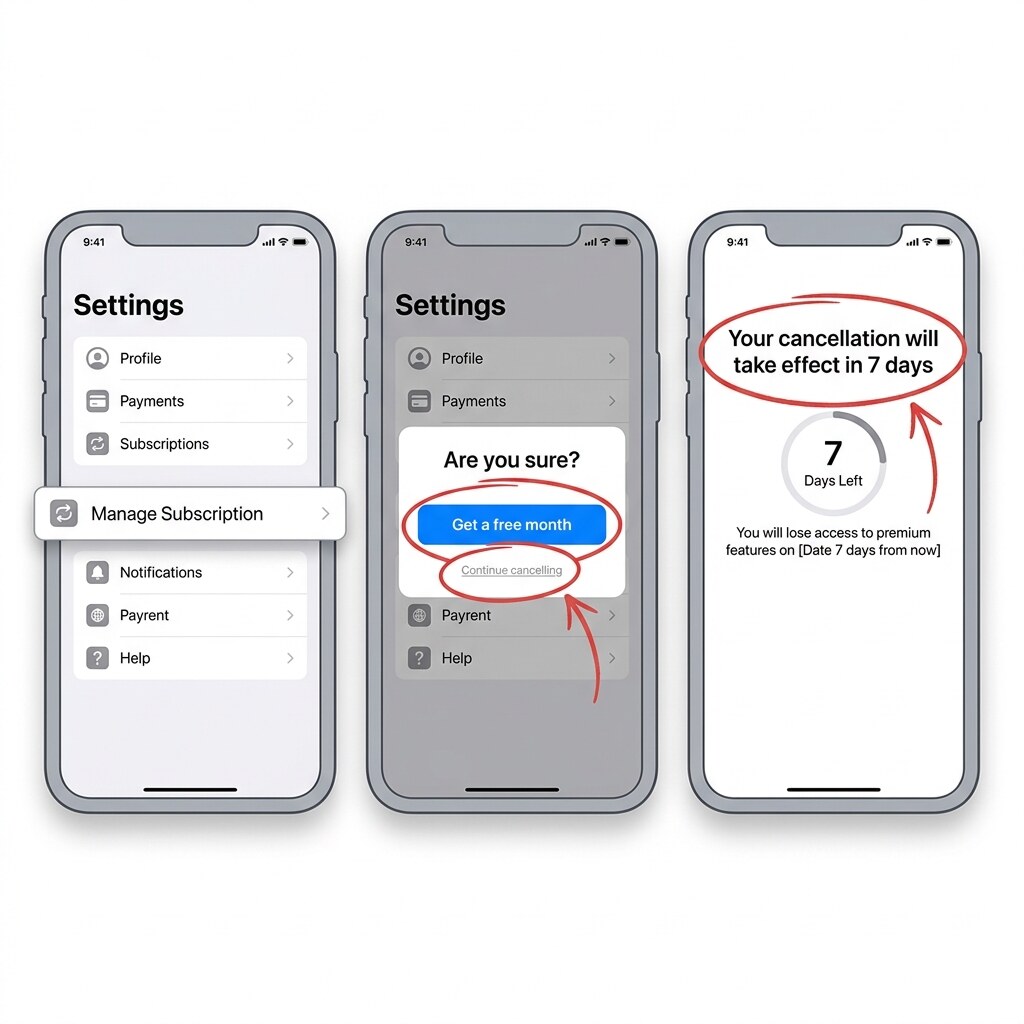

Apple App Store and Google Play both require clear pricing at subscription purchase and a standardized path to cancel (Apple: Settings, Subscriptions; Google: Play Store, Payments and Subscriptions). Cancelling there reliably stops the billing. What it does not do is trigger a refund for months already paid, and it does not cancel in-app memberships that bypass the App Store billing system, which some apps run.

Practical move before you cancel: open the app first, look for an in-app cancel flow, take a screenshot. Then kill it at the OS level as a backup. Check your statement the following month to confirm the charge actually stopped.

Subscription-Free Alternatives

If the subscription math does not work for you, the category has options:

- Klover. Free tier, ad-supported, limits unlock with points. Caps at $200.

- MoneyLion Instacash. Standard Instacash up to $500 has no monthly fee. Turbo delivery ($0.49 to $8.99) is optional. The subscription only kicks in if you want RoarMoney ($1/mo) or Credit Builder Plus ($19.99/mo).

- Cash App Borrow. Available to select Cash App users with fixed flat fees rather than a subscription. The trade-offs across fee structures are the focus of our APR vs. origination vs. subscription breakdown.

- Your bank's own advance product. Chase, Wells Fargo, Bank of America, and several regional banks now offer small-dollar advances capped under 36% APR with no recurring fee.

The One-Sentence Test

Take a look at your last 90 days of app activity. Count the advances. Multiply the monthly fee by three. Divide. If the resulting per-advance cost, plus any expedite or flat fee you paid on top, is more than 10% of your average advance amount for a two-week repayment, the subscription is not working for you. Cancel this billing cycle, not next.

What This Means for Your Balance

Subscription loan apps are not scams. They are financial products with real features and a fixed-cost pricing model that rewards frequent use. The problem is that frequent use is also the pattern most associated with cash-flow stress, which is the exact condition where paying $8.99 to $19.99 a month for access to $100 advances becomes a tax on being short. Run the break-even math once a quarter. If the numbers do not clear, the cheapest subscription is the one you cancel.

Common questions from readers.

Short answers to the questions we get by email after this article publishes.

01 Are loan app subscription fees counted as part of the APR?

Not under current federal law. The CFPB's December 23, 2025 Advisory Opinion and the withdrawal of its 2024 proposed interpretive rule leave subscription fees outside the TILA finance-charge definition. Apps can legally advertise 0% APR on advances while charging a monthly membership, which is why break-even math has to be done by the user.

02 How do I calculate the real cost of a Brigit or Dave subscription?

Divide the monthly fee by the number of advances you take that month, then add any expedite or flat advance fee. Divide that per-advance cost by the advance amount, multiply by 365 divided by your repayment window in days, multiply by 100. That is the effective APR attributable to the subscription on a single advance.

03 How many advances do I need per month for a $8.99 subscription to be worth it?

Roughly three to four advances per month is the break-even zone on Brigit Plus for a user paying no other fees. Below three, the monthly fee dominates and effective per-advance cost stays high. Above four, the fee dilutes quickly, and the subscription starts to look rational compared to per-advance pricing on non-subscription apps.

04 Can I cancel a loan app subscription easily?

Apple and Google enforce standardized cancellation paths for App Store and Play Store subscriptions, and those paths reliably stop billing. Some apps also run in-app memberships that bypass platform billing, so check both. The FTC's November 2023 action against Brigit centered partly on allegations about cancellation clarity, which Brigit disputed and settled.

05 What is the cheapest loan app if I only borrow once in a while?

For occasional borrowers, Klover (free, ad-supported, up to $200) and MoneyLion Instacash standard (no monthly fee, optional Turbo delivery) typically beat subscription apps. A $8.99 monthly Brigit fee on a single $150 advance works out to roughly 5.99% of the loan in fixed cost before any delivery fee, which is hard to justify for low-frequency use.

Related articles

Earned Wage Access: Employer-Partnered vs. Direct-to-Consumer

Best Loan Apps for Gig Workers and the Self-Employed