Apple's App Store Review Guidelines and Google Play's Personal Loans policy both cap the annual percentage rate on loan apps at 36% including all fees, both prohibit requiring full repayment within 60 days, and both have pulled apps for violating those rules. The practical difference: Apple enforces mostly through pre-review gating (an app is blocked before it ever goes live), while Google Play leans on reactive takedowns after user complaints or outside research. That asymmetry is why certain loan apps show up on an Android phone but not on an iPhone, and why some apps stay on Google Play for months after they arguably should have been pulled.

Two private companies now function as the most important consumer-lending regulators in the country. Not the CFPB, not the state AGs, not Congress. Apple and Google. I have been watching that shift happen since 2019, and it deserves a lot more attention than it gets.

Two companies, one de facto US lending rule

Only about 18 states plus DC have a 36%-or-lower APR cap on small-dollar consumer loans. In the other 30-plus states, triple-digit APRs are legal, and payday lenders operate openly on Main Street. But pull out your phone, open the App Store or Google Play, and the ceiling collapses to 36%. Try to distribute a mobile app that charges 199% APR. Neither store will let you through the door.

That is the part people miss. The Military Lending Act capped APRs at 36% for active-duty service members and their families back in 2006. Since 2019, Apple and Google have functionally extended a similar cap to everyone who wants to borrow through an app. Congress never voted on this. Most consumers have no idea it's the rule. But it is the rule, and it shapes which products actually exist.

How the 36% cap works on each store

Apple App Review Guideline 1.4.3 is the operative text for the App Store. It says, in plain language, that loan apps may not charge APR above 36% including all fees, may not require full repayment within 60 days, and must clearly disclose the APR and payment due date in the app. Apple clarified the guideline again in November 2025, tightening the disclosure language.

Google Play's Financial Services policy covers the same ground for Android. The Personal Loans section sets the 36% ceiling. A policy update effective May 28, 2025 extended the rule to line-of-credit apps, closing a loophole that some fintechs had been using to structure products as revolving credit rather than installment loans. Google Play's policy also explicitly bars personal-loan apps from accessing contacts, photos, precise location, external storage, call logs, or SMS.

| Rule | Apple App Store | Google Play |

|---|---|---|

| Max APR | 36% including fees | 36% including fees |

| Min repayment period | No full repayment within 60 days | No full repayment within 60 days |

| Disclosure in listing | APR, payment due date | APR, cost example, repayment terms, privacy policy |

| Data-access limits | General App Review privacy rules | Explicit ban on contacts, photos, precise location, external storage, call logs, SMS |

| Line-of-credit coverage | Under 1.4.3 | Added explicitly May 2025 |

| Enforcement style | Pre-review gate plus reactive takedown | Primarily reactive |

The data-access crackdown and why it matters to you

Before April 2023, it was standard for loan apps (especially overseas ones) to request access to your entire contacts list on install. The reason wasn't fraud prevention. It was collections leverage. If you missed a payment, the app would spam your mother, your boss, and your ex with demands. That practice was rampant in predatory lending ecosystems in India, Nigeria, and Latin America, and it was bleeding into US-targeted apps.

Google Play's April 2023 policy update banned personal-loan apps from requesting photos, contacts, and precise location. Apple tightened its equivalent rules shortly after. The effect was real and immediate: a wave of apps either restructured or got pulled. The most famous case was RapiPlata, flagged by Check Point Research in February 2025 for exfiltrating SMS messages, call logs, and calendar data on first launch (a pattern we break down in our loan-app data privacy guide, and a tell to verify against in how to spot a fake loan app). Both stores removed it, but only after roughly 150,000 US and Latin American users had already installed it.

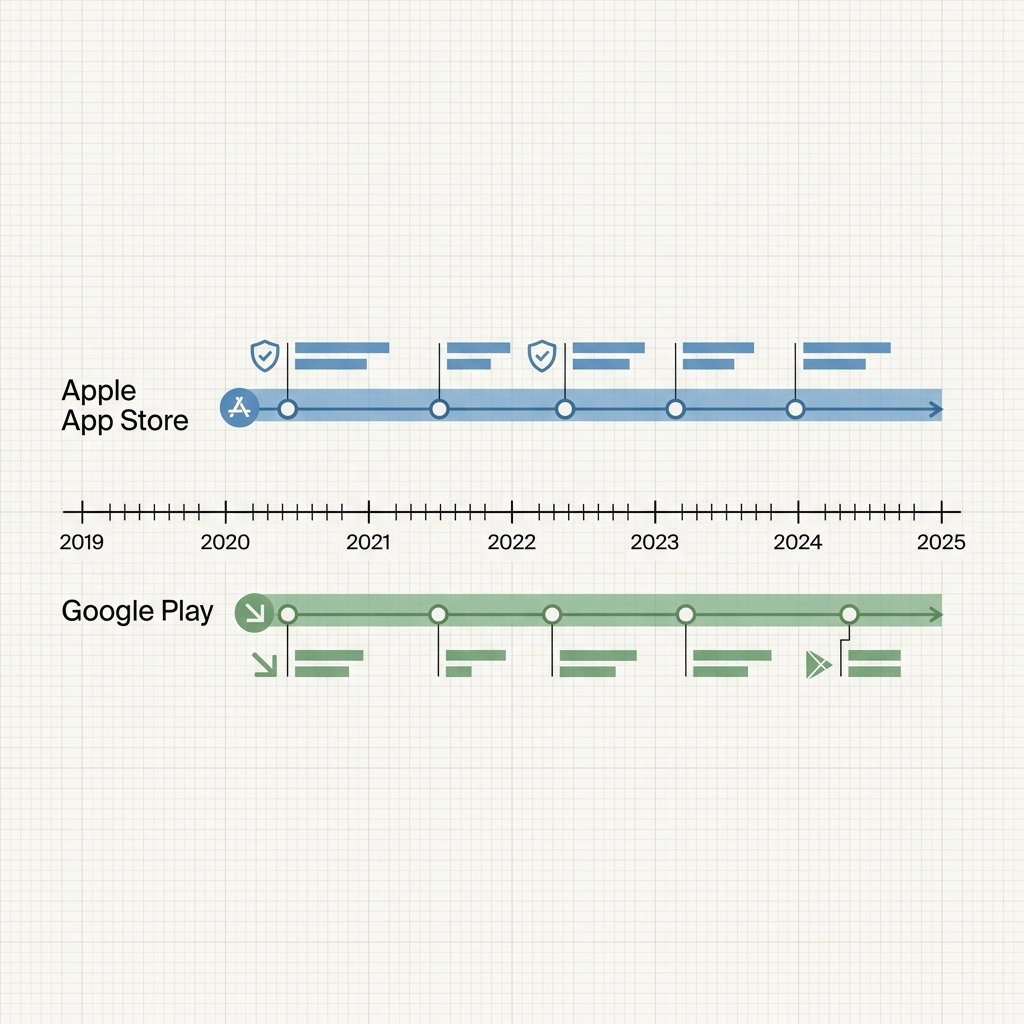

A timeline of enforcement, 2019 to 2026

- October 2019. Google Play introduces the 36% APR ban for US personal-loan apps. First reported by the Wall Street Journal.

- 2020 through 2022. Apple's Guideline 1.4.3 solidifies. Enforcement tightens quietly through pre-review rejections.

- April 2023. Google Play restricts personal-loan apps from accessing photos, contacts, and precise location.

- February 2025. RapiPlata pulled from both Apple and Google stores after Check Point Research disclosure.

- April 2025. Google Play announces the line-of-credit expansion, with compliance required by May 28, 2025.

- November 2025. Apple clarifies Guideline 1.4.3 loan disclosures and reaffirms the 36% ceiling.

Apps that have been pulled, and what happens to your open balance

If an app you have an open loan with gets removed from the store, your legal obligation to repay does not vanish. The loan contract survives the delisting. What changes is your ability to manage the account through the mobile interface. You may need to use the lender's website instead, or in some cases a new replacement app.

A few things to do if this happens to you:

- Download a copy of your current loan agreement, payment history, and any disclosures from the app before it stops working.

- Confirm the lender's continuing contact information through NMLS Consumer Access (nmlsconsumeraccess.org), not through a link the lender sends you.

- Do not start making payments to a new account or a new payment processor without independently verifying the legitimacy of the transition. Delistings are prime fishing windows for scammers pretending to be the original lender.

- If the lender disappears entirely and stops accepting payments, keep your records and report to the CFPB. A delisting is not permission to stop paying, but an unreachable lender is a complicated situation that often ends with the debt being sold to a collector. You want the paper trail.

The tip and subscription loophole

Here is the awkward part of the story. The 36% rule measures "APR including fees." Tip-based apps (Earnin, Cleo, Klover) and subscription-based advance apps (Brigit, MoneyLion) operate in a gray zone that both stores have tolerated. We dig into the math in the true cost of tip-based loan apps and whether subscription fees are worth it. The argument is that a "voluntary" tip is not a fee, and a monthly subscription that unlocks other features is not a per-loan charge. Under that framing, these apps are technically compliant.

Consumer advocates, the California DFPI, and the New York Attorney General disagree. The NY AG's April 2025 suit against MoneyLion and DailyPay alleges effective APRs "frequently up to 750%" once tips and subscription fees are counted. The California DFPI proposed treating tips as charges subject to state fee caps. The federal CFPB, in a December 23, 2025 Advisory Opinion, went the opposite way and held tips are not finance charges under TILA.

Apple and Google have not publicly resolved this question. The apps remain in both stores. If state regulators win, that may change. For now, the 36% ceiling has a visible leak, and the leak is intentional.

The bank-partner loophole (and why it's smaller than it looks)

Under federal preemption, a state-chartered bank can export its home-state interest rate to borrowers in other states. Some fintech lenders partner with banks in states like Utah that lack a meaningful usury cap, structurally allowing APRs above 36%. These "rent-a-bank" arrangements are legally valid under current federal precedent, though they are contested.

The catch: an app distributed through the App Store or Google Play still has to pass the 36% review regardless of the underlying bank partnership. The legal validity of the loan and the app-store's willingness to carry the app are two different questions. Most rent-a-bank high-APR products therefore route through the web or through direct-to-consumer payment channels, not through mobile apps. The app-store policies have successfully pushed the most expensive lending off the phone, even when it remains legal elsewhere.

What this means for you, practically

Three takeaways if you're borrowing through an app:

- If you can install it from the App Store or Google Play and the APR is disclosed in the listing, you are probably looking at a loan capped at 36%. That is a meaningful floor of consumer protection that did not exist ten years ago.

- If a "loan app" has to be sideloaded from a web page or an APK link, the 36% ceiling does not apply. Treat that as a serious warning sign and verify the lender through NMLS before going further.

- If you use a tip-based or subscription-based advance app, the 36% rule is not protecting you. Calculate the effective APR yourself and decide whether the product is worth it.

A loan app that passes both store reviews and has an active NMLS Consumer Access record is generally your safest starting point. If something does go wrong, you can also file a complaint with the CFPB.

Common questions from readers.

Short answers to the questions we get by email after this article publishes.

01 Why is a loan app on my girlfriend's Android but not on my iPhone?

Most likely the app has not passed Apple's pre-review gate, or it was rejected under Guideline 1.4.3 and is waiting on a resubmission. Google Play's enforcement is mostly reactive, so apps can go live and later be pulled, while Apple tends to block before launch. It can also reflect a developer choosing to launch on one platform first to test compliance before filing with the other.

02 Does the 36% APR cap apply to tips on Earnin or Dave?

Officially, neither store has ruled publicly that voluntary tips count as fees under the 36% rule. Apps structured around tips and subscriptions have been permitted on both platforms. State regulators in California and New York argue tips should count as interest and have opened enforcement actions. The CFPB's December 2025 Advisory Opinion went the opposite direction federally. The question is unresolved and very much live.

03 What happens to my open loan if the app gets pulled?

Your repayment obligation survives the delisting. The loan contract is a legal agreement that doesn't vanish when the distribution channel does. Download your payment history and loan documents before the app stops working, verify the lender's current status through NMLS Consumer Access, and do not send payments to a new account until you have independently confirmed the transition is legitimate.

04 Can a loan app charge more than 36% APR legally?

In about 30 US states, yes, traditional storefront lenders and web-only lenders can legally charge triple-digit APRs under state law or through federally preempted bank-partner structures. What the app-store policies do is prevent those products from being distributed through iOS or Android apps. The 36% ceiling is a distribution rule, not a usury law, and it applies only to mobile-app channels.

05 Who do I complain to if a loan app is violating App Store or Google Play policy?

Report to Apple through the "Report a Problem" link on the App Store listing, or to Google through the "Flag as inappropriate" link on the Google Play listing. Both stores also accept policy-violation reports through their developer support channels. In parallel, file with the CFPB at consumerfinance.gov/complaint and with your state AG's consumer-protection office, which tends to move faster on predatory-lending complaints than the stores do.