The 50-state patchwork in one paragraph

The United States does not have a single federal cap on consumer-loan interest rates. The Military Lending Act caps APR at 36% for active-duty service members and their dependents, and Apple App Store and Google Play both enforce a 36% all-in ceiling for loan apps in their stores. Outside those two backstops, the cap that actually applies to you depends on the state you live in and the structure the lender uses to reach you.

Eighteen states plus the District of Columbia cap consumer loans at or below 36% APR. Several states cap them at 16% to 25% (New York's civil and criminal usury caps). A handful of states, notably Texas, have a low constitutional rate ceiling but allow a separate licensee class to layer on uncapped fees, producing a published APR over 500%. The same loan app, with the same legal structure, can be cheap in one state and ruinous in another.

The four state archetypes

1. Hard 36% cap states. Connecticut, Illinois, Maine, Maryland, Massachusetts, Montana, Nebraska, New Hampshire, New Jersey, New Mexico, New York (effectively), North Carolina, Oregon, Pennsylvania, South Dakota, Vermont, Washington, West Virginia, plus DC. In these states, most high-APR app-based products either restructure their pricing to fit, partner with an out-of-state bank to attempt federal preemption, or geofence the state entirely. If you live in one of these and an app says "not available in your state," the cap is doing its job.

2. Civil/criminal usury states. New York is the cleanest example. Civil usury under General Obligations Law 5-501 is 16% APR; criminal usury under Penal Law 190.40 is 25%, a Class E felony. NYDFS's 2020 "true lender" position treats bank-partner fintechs as the real lender for state-law purposes, which is why OppLoans, NetCredit, and most tribal-affiliated installment products do not lend to New York residents.

3. Workaround states. Texas is the archetype. The state constitution caps contractual interest at 10%, but Finance Code Chapter 393 lets Credit Access Businesses (CABs) charge uncapped broker fees on top of that interest. The third-party lender collects 10%, the CAB collects the fee, and the combined APR runs 400% to 600%. California is a partial workaround state too, though AB 539 closed most loopholes in the $2,500 to $10,000 band by capping at 36% plus the Federal Funds Rate.

4. Permissive states. Utah, Idaho, Wisconsin, and Delaware are the most common home states for the bank charters fintechs use to export rates into the rest of the country. The federal preemption argument lets a state-chartered bank in Utah originate a 100%+ APR loan and assign it to a fintech servicing borrowers in stricter states. Whether that actually holds depends on the strict state's "true lender" stance, which is now actively contested.

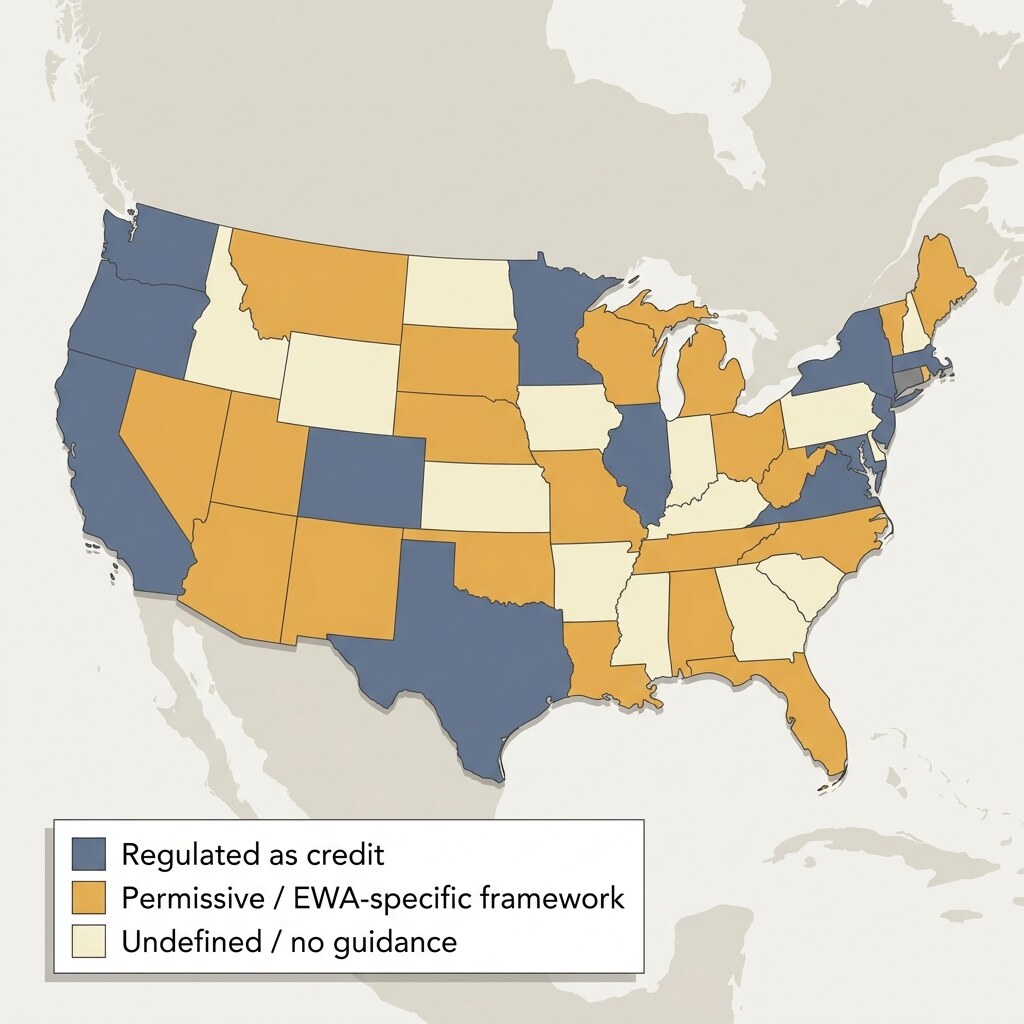

EWA registration: the new state-by-state line

Earned wage access has its own state map. A cluster of states has written EWA-specific statutes that classify covered products as non-loans and require registration: Nevada (SB 290, July 2024), Missouri (2023), Kansas (July 2024), Wisconsin, South Carolina, Arkansas, Utah (2025), Connecticut (2025), Louisiana (2025). The opposite stance shows up in California, where DFPI's Income-Based Advances rule (effective February 15, 2025) treats certain "tips" as charges subject to fee caps and required several apps to restructure. New York's April 2025 AG suit against DailyPay and MoneyLion is testing whether tips function as usury in the state.

How to use this for your specific borrow

Before you tap install, do three checks. First, verify the lender's state license in NMLS Consumer Access (nmlsconsumeraccess.org). If they do not appear with an active license in your state, they cannot legally lend to you there. Second, read the in-app state-specific disclosure screen at the final loan-agreement page; the marketing screen lies about availability more often than the disclosure does. Third, calculate the all-in APR including any tip, expedite fee, or prorated subscription, and compare it to your state's cap. If the math comes in above the cap, ask the lender how they justify it; the answer should reference a specific federal preemption pathway or licensee class.

Where to dig deeper

Long-form state guides we have already published: California: AB 539 and DFPI, New York: 16% civil and 25% criminal usury, and Texas: the 10% constitutional cap and the CAB structure. More state guides are in the editorial queue and roll into this hub as they publish.