Here is the shortest honest answer: a cash advance app like Dave, Earnin, or Brigit pulls a smaller, faster debit from your checking account on payday, while a payday loan sends a larger ACH (automated clearinghouse) debit on a scheduled due date and, if it bounces, may try again and again. Both products can trigger overdraft fees. Both can leave you with less money than you started with. The difference shows up in the timing, the fee structure, and what happens when the money is not there.

You are probably reading this because you have already used one or the other, felt the sting, and want to know which one does less damage next time. Fair question. Let's walk through it the way your bank statement actually shows it.

Two Products, One Checking Account

A payday loan is a small, short-term loan (usually $100 to $500, two-week term) from a storefront lender or an online lender that takes your post-dated check or your ACH authorization as the promise of repayment. The classic fee is $15 per $100 borrowed over 14 days. The Consumer Financial Protection Bureau (CFPB) pegs that at a 391% annual percentage rate (APR), the yearly cost of borrowing expressed as a percent.

A cash advance app is a mobile app that fronts you a small amount (usually $20 to $500) against your next paycheck. You link your checking account through a data connector like Plaid, the app watches your direct deposit, and it debits itself on payday. The app does not charge "interest" in the traditional sense. It charges a subscription (Brigit is $9.99 a month, which we break down in whether subscription fees are worth it), an expedite fee to get the money in minutes instead of days ($1 to $5.99 is typical, with a $3.18 average per the CFPB), and, on some apps, a suggested tip.

Two different products. One shared feature: both live inside your checking account and both get first dibs on your money when it arrives.

Payday Loan Timing: The ACH Pull, the Rollover, and the Re-Attempt

When you take out a payday loan, you sign an ACH authorization that lets the lender pull the full loan amount plus the fee on your due date. That due date is usually your next payday, 10 to 14 days out.

Here is what typically happens:

- Your paycheck direct-deposits at, say, 12:01 a.m. Friday.

- The lender's ACH debit posts the same day, sometimes before other pending items.

- If the balance covers it, the debit clears and the loan is gone.

- If the balance does not cover it, the bank may return it NSF (non-sufficient funds), hitting you with a fee that averages $27 to $35.

- The lender then tries again. And possibly again. Each failed attempt can cost you another NSF fee at your bank.

The CFPB's Payday Rule payment provisions took effect March 30, 2025. After two consecutive failed ACH attempts, a covered lender is supposed to stop and get fresh authorization before trying a third time. The Bureau also said it would not prioritize enforcing that rule, which means your protection on paper is stronger than your protection in practice. Read that twice.

And rollovers? The CFPB has found more than 80% of payday loans are reborrowed within a month, and nearly one in four are reborrowed nine times or more. If you roll a $300 loan four times at $45 per rollover, you have paid $180 in fees and still owe the $300.

Cash Advance App Timing: The Deposit Watch and the Auto-Debit

Cash advance apps work differently on the front end, but similarly on the back end. You link your checking account. The app studies your deposit pattern (how often, how much, from where) to estimate the size of advance you can handle. When you request the advance, you get the money either in 1 to 3 business days for free, or in minutes for an expedite fee.

On repayment day, the app watches for your next direct deposit. When it lands, the app pulls its advance back, usually the same day, sometimes within an hour. You do not get a chance to move that money somewhere else first.

This is where people get hurt. A few common traps:

- Pull-before-post timing. If your direct deposit is "pending" but not yet available, and the app's debit hits first, your balance can dip negative. Overdraft fee. Same paycheck, less money.

- Stacked advances. If you have advances on two apps (say, Dave and Brigit), both try to repay themselves on the same payday. One clears. The other overdrafts.

- Unexpected subscription. The app's monthly fee posts on its own schedule. If it hits the week before payday, that is another $9.99 your balance was not planning on.

Earnin, Dave, and Brigit all frame their advances as "no interest." Technically true. Practically misleading, because the expedite fee plus the subscription plus an optional tip compresses into a 7-day or 14-day cost that, when you do the APR math, often lands higher than a credit card and sometimes higher than a payday loan.

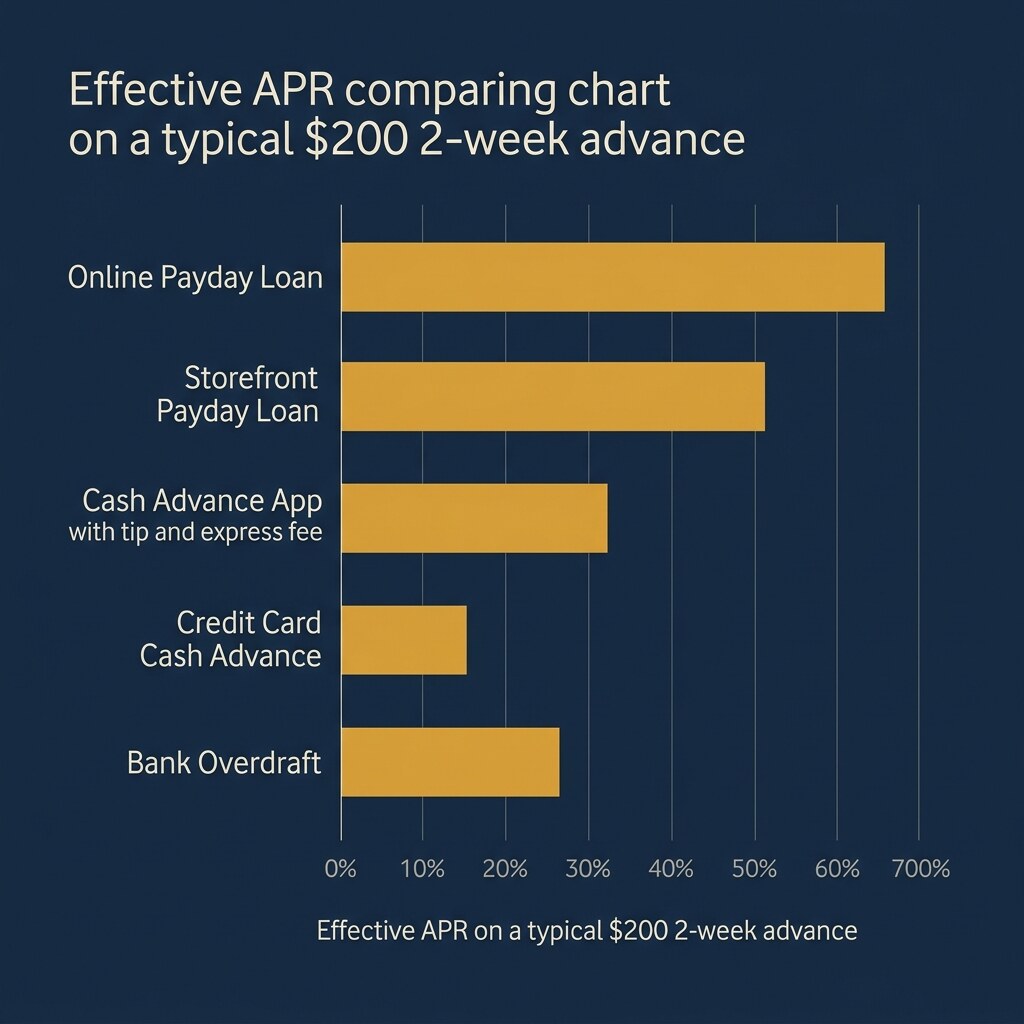

The True Cost, Side by Side

Let's run the numbers on a $200 advance. Real scenarios, not best-case marketing claims.

| Product | Amount | Term | Fees paid | Total repaid | Effective APR |

|---|---|---|---|---|---|

| Storefront payday loan | $200 | 14 days | $30 ($15 per $100) | $230 | 391% |

| Dave ExtraCash (expedited, $3 tip) | $200 | 14 days | $1 sub + $4.99 expedite + $3 tip = $8.99 | $208.99 | 117% |

| Earnin (expedited, $5 tip) | $200 | 7 days | $3.99 expedite + $5 tip = $8.99 | $208.99 | 234% |

| Brigit Plus (instant) | $200 | 14 days | $9.99 monthly | $209.99 | 130% |

| Direct-to-consumer EWA average (CFPB) | Any | Per advance | Expedite + tip | Varies | 205% average |

Two things stand out. First, the apps are usually cheaper than a storefront payday loan, but not by as much as their marketing suggests. Second, the shorter the advance period, the higher the APR even when the dollar cost is low. A $5 fee on a 7-day advance is mathematically expensive, even if it feels like pocket change.

When the "Fee-Free" App Actually Costs More Than a Payday Loan

There is a specific scenario where the app wins on fees and still loses you more money than a payday loan would have. It looks like this:

You take a $100 advance from an app on Tuesday. You pay $4.99 to expedite. On payday Friday, your direct deposit is still processing when the app's $104.99 debit hits. Your balance goes negative by $80. Your bank charges a $35 overdraft fee. Then your auto-pay for Netflix hits, and that is another $35.

Total out of pocket on a $100 advance: $4.99 expedite + $35 overdraft + $35 cascading overdraft = $74.99. That is a 3,900% APR on a 3-day advance. You would have done better walking into the payday storefront.

The CFPB reported that in 2024, US consumers paid $12.1 billion in overdraft and NSF (non-sufficient funds) fees, and 79% of that was paid by 9% of consumers. If you are in that 9%, a cash advance app is not a cost-free product. It is an overdraft trigger with a friendly interface.

What the CFPB Payday Rule and the FTC's Dave Case Mean for You

Two regulatory items to know, because both affect what these products can legally do to your bank account.

CFPB Payday Rule, effective March 30, 2025. Lenders making loans above 36% APR cannot keep re-attempting an ACH debit after two failed tries without asking you for fresh authorization. The Bureau has said it will not prioritize enforcement, so your best defense is still your own bank. You can revoke an ACH authorization in writing at any time. Your bank will then block the debit if you give them the revocation notice.

The FTC v. Dave, Inc. case, filed in November 2024 and referred to the Department of Justice in December 2024, alleges Dave advertised "up to $500" advances most users never qualified for, hid Express Fees ranging $3 to $25, and assigned default tips of 10% to 20% that many users did not realize were optional. The case is still pending. Whether or not Dave is found liable, the complaint is a good reading of what to look for in any cash advance app you evaluate.

Red Flags Before You Link Your Bank Account

A short checklist you can run in about 90 seconds before you hit "connect":

- Can you find the full fee schedule before signing up? If expedite fees, subscription costs, and tip defaults are not on one page, that is a red flag.

- Is there a clear $0 tip option, or do you have to dig through menus to find it?

- Does the app state whether it will re-attempt a failed debit, and how many times?

- Can you revoke ACH authorization inside the app, or only by emailing support?

- Is the company state-licensed where you live, and is that license posted?

- Does the app report on-time repayment to any credit bureau?

How to Actually Compare APR on a 7-Day Advance

Here is the formula that strips out the marketing: APR = (total fees / amount borrowed) x (365 / days of advance) x 100.

A $100 advance, $5.99 expedite fee, $3 tip, 7 days until repayment:

($8.99 / $100) x (365 / 7) x 100 = 468% APR.

Run that math on any advance before you tap accept. If the number shocks you, trust it.

So, Which Is Worse?

A payday loan is almost always more expensive in absolute dollars. A cash advance app is almost always cheaper per transaction, but more habit-forming, because the fees feel small and the UX makes it easy to take another advance right after the last one cleared. CFPB data shows direct-to-consumer app users average 36 advances a year. California DFPI data says the same. That is not a borrowing pattern. That is a payment schedule.

If you have to pick, pick once. Borrow the smallest amount you can live with, pay it back on the first payday, and delete the app. If you find yourself reopening it the following Tuesday, the app has stopped being a tool and started being a trap (and a credit-union Payday Alternative Loan is usually the cheaper exit).

Common questions from readers.

Short answers to the questions we get by email after this article publishes.

01 Can a cash advance app overdraft my account?

Yes. If the app's repayment debit hits before your direct deposit fully posts, or before other pending transactions clear, your balance can go negative and trigger an overdraft fee from your bank. This is one of the most common borrower complaints about Dave, Earnin, and Brigit, and the risk is highest when you have multiple apps debiting on the same payday.

02 Do cash advance apps check my credit?

Most do not run a hard credit check. Apps like Dave, Earnin, Brigit, and MoneyLion Instacash underwrite using bank-transaction data instead, looking at deposit cadence, account balance history, and spending patterns. The upside is no credit score requirement. The downside is that on-time repayment usually does not build your credit either, because most of these apps do not report to Experian, Equifax, or TransUnion.

03 Is a payday loan ever cheaper than an app?

In raw dollar terms, rarely. A storefront payday loan typically costs $15 per $100 borrowed over 14 days. A cash advance app usually lands between $3 and $12 all in. Payday loans can look cheaper only if you trigger overdraft fees because of an app's aggressive repayment timing, or if you stack subscription fees from multiple apps you forgot to cancel.

04 Can I stop a lender from trying to debit my account?

Yes. You have the right to revoke ACH authorization at any time by sending a written notice to the lender and a copy to your bank. The CFPB provides a sample revocation letter at consumerfinance.gov. Your bank may still charge a stop-payment fee, but the debit will be blocked. Revoking authorization does not cancel the debt itself.

05 Why do apps ask for a tip?

Tips let apps collect revenue without calling it interest, which keeps them outside Truth in Lending disclosure rules in most states. The FTC's pending complaint against Dave alleges default tip settings of 10% to 20% were applied without clear user consent. Always check for a $0 tip option before you confirm an advance, and do the APR math including the tip.