Short answer, because you are probably in a hurry: most cash advance apps (Dave, Earnin, Brigit's free tier, Klover, Chime SpotMe) do not show up on any credit report, at any of the three bureaus. Credit-builder products layered on top of those apps (Brigit Credit Builder, MoneyLion Credit Builder Plus, Self, Kikoff) usually report to all three. Installment loans from apps like Possible Finance, OppLoans, SoFi, Upgrade, and Upstart almost always report. Which means whether your loan app helps, hurts, or does absolutely nothing to your credit depends entirely on which product inside the app you are using.

If you downloaded Dave to cover a $300 car repair and you are hoping that paying it back on time will nudge your score up, I have news you need to hear. It will not. Not because you did anything wrong, but because Dave does not tell the credit bureaus you exist. Let's walk through which apps actually report, to whom, and what that means for your score.

The Short Answer, One More Time With Detail

Your credit report has three separate versions, one from each bureau: Experian, Equifax, and TransUnion. A "bureau" is a private company that collects credit history from lenders who voluntarily furnish it under the Fair Credit Reporting Act. Nobody is required to report. Some lenders report to all three. Some report to one. Most cash advance apps report to none.

That creates a three-layer reality inside the loan-app world:

- Layer 1: Nothing reported. Pure cash advance and earned wage access (EWA) products. Your repayment history is invisible to the bureaus.

- Layer 2: Soft pull at onboarding, nothing else. The app checks something at signup (a soft credit inquiry, which does not affect your score, or an income verification through Plaid) but does not furnish ongoing data.

- Layer 3: Full reporting. Installment loans and credit-builder accounts that report on-time and late payments monthly to one or more bureaus.

What Each Bureau Actually Receives

Here is the cell-by-cell breakdown, verified against each app's current disclosure pages. Policies change, so when you are ready to apply, spot-check the lender's disclosure page one more time.

| App / Product | Experian | Equifax | TransUnion | Pull type |

|---|---|---|---|---|

| Dave ExtraCash | No | No | No | None on advance |

| Earnin | No | No | No | None |

| Brigit Instant Cash | No | No | No | None |

| Klover | No | No | No | None |

| Chime SpotMe | No | No | No | None |

| Brigit Credit Builder | Yes | Yes | Yes | Soft |

| MoneyLion Credit Builder Plus | Yes | Yes | Yes | Soft |

| Self Credit Builder | Yes | Yes | Yes | Soft |

| Kikoff | Yes | Yes | Yes | Soft |

| Possible Finance | Yes (varies) | Yes (varies) | Yes | Soft |

| Upgrade personal loan | Yes | Yes | Yes | Hard at funding |

| SoFi personal loan | Yes | Yes | Yes | Hard at funding |

| Upstart personal loan | Yes | Yes | Yes | Hard at funding |

| OppLoans installment | Yes | Yes | Yes | Soft (alt bureau) |

Notice the pattern: cash advance products are consistent across all three bureaus (none of them see anything), and installment or credit-builder products are also consistent (usually all three). The confusing middle is products like Possible Finance, where reporting varies by state because the product's legal structure changes from one state to the next.

Soft Pull vs. Hard Pull at Application

Two quick definitions, because they sound the same and they are not.

A soft pull is a credit check that does not affect your score. You see it when you log into Credit Karma, when a card issuer sends you a pre-qualified offer, or when a loan app checks your credit to see if you are in the ballpark. Soft pulls are invisible to anyone else checking your credit.

A hard pull is a credit check that happens when you formally apply for a loan or credit line. It shows up on your report, stays there for two years, and typically drops your FICO score by 2 to 5 points. One hard pull is nothing to worry about. Six in a month will get noticed.

Cash advance apps like Dave, Earnin, and Brigit do not run either. They use bank-transaction data through Plaid instead (we cover what that data trail looks like in loan app data privacy: what they collect). Credit-builder products run a soft pull at signup. Installment loans from Upstart, SoFi, and Upgrade do a soft pull when you "check your rate" and a hard pull if you accept the offer and move to funding.

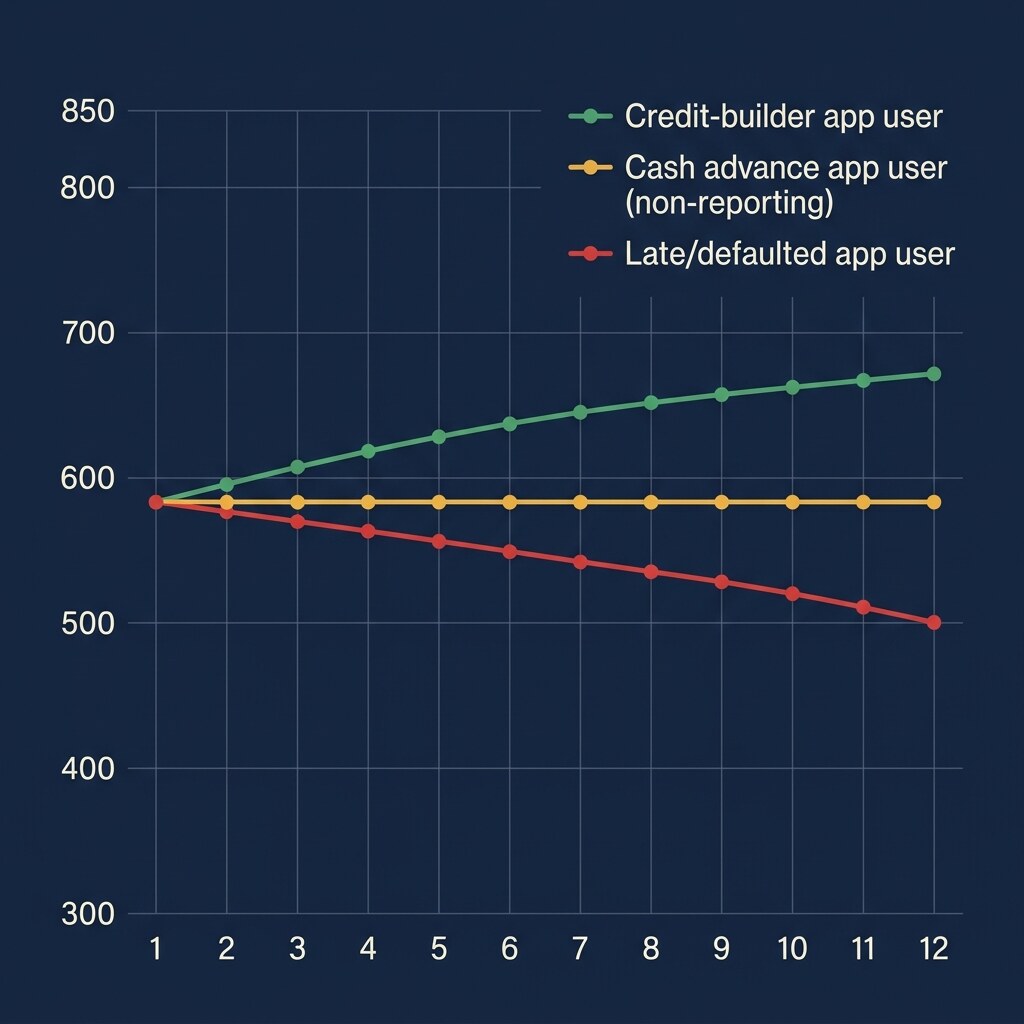

What Happens When You Repay on Time

On a credit-builder or installment product, on-time payments are the whole point. Each on-time monthly payment shows up as a positive tradeline on whichever bureaus the lender furnishes to. Payment history is 35% of your FICO score, the single biggest factor. Six to twelve months of on-time payments on a small installment loan can meaningfully move a thin-file score.

On a pure cash advance app, on-time repayment does nothing for your credit. Nothing. You can pay back 40 Earnin advances in a row, on time, without a single hiccup, and a mortgage lender reviewing your file will have no idea you ever borrowed a dollar. This is why people ask me, "I've been using Dave for a year and my score hasn't moved, is that normal?" Yes. Completely normal. It is the design.

What Happens When You Default

This is where the reporting picture shifts in ways most people do not expect.

If you default on an installment loan or a credit-builder account, the missed payments hit your credit report immediately, usually after 30 days late. After 120 to 180 days, most lenders charge off the account (write it off as a loss) and sell it to a collections agency. That collections account is its own separate negative item on your report. Both the original tradeline and the collection can stay on your report for up to seven years.

Cash advance apps (the kind we compare against payday loans) are different. Because they do not report on-time activity, you might assume they also do not report defaults. Mostly true, but with a catch. Dave, Brigit, MoneyLion, and Possible Finance have all been reported by borrowers to sell unpaid advances to third-party collections agencies. Once that collections agency reports to a bureau, the debt can show up on your credit report even though the original advance never did. Paying back an advance late is usually fine (you just cannot borrow again). Never paying it back at all can still end up on your report through the back door.

How to Pick a Loan App If Building Credit Is Your Real Goal

If your goal is a loan, pick for cost and speed. If your goal is credit, pick for reporting. They are not the same decision.

For credit building specifically, the short list is:

- Self Credit Builder Account. Structured as a savings-backed installment loan. Reports monthly to all three bureaus. Good for people with no credit or thin credit.

- Kikoff. $5 a month. Reports to all three bureaus. Small credit line, built specifically to add positive payment history.

- MoneyLion Credit Builder Plus. $19.99 a month. Reports to all three bureaus. Bundles a small installment loan with banking features.

- Brigit Credit Builder. Layered on top of the Brigit Plus subscription. Reports to all three bureaus.

- Possible Finance installment. Reports to two or three bureaus depending on your state. Good if you need the cash and the credit build in the same product.

One rule I give every student in my community-college workshop: do not pay a subscription fee for credit building if you are not actually going to use the product. $19.99 a month for a year is $239.88. Self's annual cost is closer to $125. Match the product to the habit you will actually keep.

How to Check Your Report for Free

The only government-authorized source for free credit reports is AnnualCreditReport.com. Since 2023 it has offered free weekly reports from all three bureaus, a permanent change from the old once-a-year rule.

Pull all three at least twice a year. Look for:

- Accounts you do not recognize (possible identity theft or old collections).

- Tradelines that should be reporting but are not (confirms the app's actual reporting behavior).

- Late payments on accounts you are current on (bureau error, dispute it under the Fair Credit Reporting Act).

You can dispute errors directly through each bureau's website. The bureau has 30 days to investigate. If you hit a wall, the CFPB takes complaints at consumerfinance.gov/complaint, and they tend to get answered fast.

The One-Line Takeaway

A cash advance app is a cash flow tool, not a credit tool. A credit-builder account or installment loan is a credit tool that sometimes also gets you cash. Pick based on the job you are trying to get done, and do not expect an app that does not report to the bureaus to change a number it does not talk to.

Common questions from readers.

Short answers to the questions we get by email after this article publishes.

01 Does using Dave hurt my credit score?

No. Dave ExtraCash advances are not reported to Experian, Equifax, or TransUnion, so using Dave, paying on time, or paying late does not affect your credit score directly. The exception is if you default on an advance and Dave sells the debt to a collections agency, which can then report the collection to a bureau and show up on your credit file.

02 Will paying off Earnin on time improve my credit?

No. Earnin does not report any activity to the credit bureaus, so on-time repayment does nothing to build your credit history or raise your FICO score. If you want on-time payments on a cash-advance-style product to help your credit, look at Possible Finance, Brigit Credit Builder, or MoneyLion Credit Builder Plus, which do report to the bureaus monthly.

03 Which bureau do most loan apps report to?

Most credit-builder loan apps (Self, Kikoff, MoneyLion Credit Builder Plus, Brigit Credit Builder) report to all three bureaus: Experian, Equifax, and TransUnion. Installment lenders like SoFi, Upstart, Upgrade, and OppLoans also typically report to all three. Pure cash advance apps report to none. Always verify with the app's disclosure page before assuming.

04 Does a soft pull on a loan app affect my credit score?

No. A soft pull (sometimes called a soft inquiry) does not affect your credit score and is not visible to other lenders checking your report. Loan apps that prequalify you or check your rate usually use a soft pull. A hard pull, which does affect your score by 2 to 5 points, happens only when you formally apply and accept a loan offer.

05 How do I get a free copy of all three credit reports?

Visit AnnualCreditReport.com, the only federally authorized free source. Since 2023, you can pull a free report from Experian, Equifax, and TransUnion every week, not just once a year. You will be asked identity-verification questions based on your credit history. Pulling your own report is a soft inquiry and does not affect your score.