If your FICO score is under 580, the loan apps most likely to approve you without a hard credit check are OppLoans, Possible Finance, Dave, Brigit, MoneyLion Instacash, and Earnin. The catch is that these apps underwrite on your bank-transaction data (direct deposit cadence, account balance, spending patterns) instead of your credit score, and they price that risk through high APRs, per-$100 fees, or monthly subscriptions. The most credit-friendly of the bunch (Possible Finance and OppLoans) report your on-time payments to the credit bureaus, so they can help rebuild. The others are cash flow tools only, and using them will not move your score up or down.

I'm going to walk you through exactly which apps genuinely approve in the sub-580 tier, what each one looks at, what you'll really pay, and how to tell a legitimate subprime app from a modern payday lender with a friendly icon. The goal is to help you borrow once, pay it off, and climb out, not settle in.

What "Sub-580" Actually Means

FICO scores run from 300 to 850. The industry bands look like this:

- Exceptional: 800 to 850

- Very good: 740 to 799

- Good: 670 to 739

- Fair (subprime): 580 to 669

- Poor (deep subprime): below 580

Under 580 is where most traditional banks auto-decline. Their underwriting models treat that tier as high default risk, and the compliance math does not support lending there at bank rates. So if you are applying with a 540 score and getting instant denials from Discover, SoFi, and your credit union, nothing is wrong with your application. You are just outside their credit box.

Bankrate's 2025 "True Cost of Subprime Credit" study estimated borrowers under 620 pay about $3,400 more per year in effective financing costs (across mortgage, auto, cards, and personal loans) than prime borrowers do. That extra cost is real, it compounds, and it is the reason getting out of the sub-580 tier is worth paying attention to even when you just need $300 for a tire.

How Cash-Flow Underwriting Works

When a loan app says "no credit check," what they usually mean is "no hard pull on your FICO score." They almost always run some kind of check. It is just a different kind.

Most sub-580-friendly apps use a data connector called Plaid (or a similar service like MX or Finicity) to read your checking account. With your permission, the app sees:

- Who pays you and how often (employer direct deposits, gig platform payouts, benefit deposits).

- How much your paychecks are and how consistent they are.

- Your average daily balance and how often you go negative.

- Large recurring bills (rent, car, utilities).

- Existing loan payments to other lenders.

Some apps also pull from an "alternative bureau" like Clarity Services (owned by Experian) or FactorTrust, which tracks small-dollar lending activity that the big three bureaus do not. That pull is usually soft, meaning it does not show up on your regular credit report and does not affect your FICO score.

The Consumer Financial Protection Bureau's Personal Financial Data Rights Rule (Section 1033), finalized in October 2024, governs how apps are allowed to access and use that bank data. You have the right to know what they are pulling, and you can revoke access at any time through your bank or through the app's data-sharing settings.

Apps That Genuinely Approve Sub-580

Verified against each company's current disclosure pages. APR and fee numbers change, so spot-check before you apply.

| App | Product type | Amount | Term | APR or fee | Reports to bureaus? |

|---|---|---|---|---|---|

| OppLoans | Installment | $500 to $5,000 | 9 to 18 months | 160% to 195% APR | Yes, all three |

| Possible Finance | Short installment | Up to $500 | Up to 8 weeks | $10 to $25 per $100 | Yes, two or three |

| Dave ExtraCash | EWA advance | Up to $500 | Until next payday | $1-$5 sub + expedite + tip | No |

| Brigit Plus | EWA advance | Up to $250 | Until next payday | $9.99 monthly | No (Instant Cash) |

| MoneyLion Instacash | EWA advance | $100 to $1,000 | Until next payday | Expedite + optional tip | No |

| Earnin | EWA advance | Up to $150/day | Until next payday | Expedite + optional tip | No |

| SoLo Funds | P2P small loan | $20 to $575 | Up to 35 days | Lender tip + platform fee | No |

A few practical notes on this list:

OppLoans is usually the right pick if you need more than $500 and want the payment reported to the bureaus to rebuild credit. Yes, 160% to 195% APR is very expensive. It is still dramatically cheaper than a storefront payday loan at 391%, it is structured as a fixed-payment installment loan, and it reports to all three bureaus.

Possible Finance is the sweet spot for small emergencies ($200 to $500). The per-$100 fee lands around $10 to $25 depending on your state, the term is a few weeks in multiple payments (not a balloon), and they report to the bureaus.

The four EWA apps (Dave, Brigit, MoneyLion Instacash, Earnin) are cash flow tools. They can bridge you to payday. They will not rebuild your credit. Do not mistake one for the other.

SoLo Funds deserves a flag. The Consumer Financial Protection Bureau filed suit against SoLo in 2024 alleging deceptive practices around tips and fees. The suit was dismissed in February 2025, but several state attorneys general (DC, Connecticut, Pennsylvania) have separately settled with or sued the company, and effective APRs on some SoLo loans have exceeded 500%. Proceed with more care than you would with Possible or OppLoans.

Apps That Claim to Help But Charge Payday-Level APRs

Some apps market themselves as "credit-friendly" or "designed for rebuilding credit" while pricing like payday loans once you do the all-in math (the CFPB Consumer Complaint Database is the fastest way to sanity-check a lender). Red flags to watch for specifically:

- Flat fees that are cheap in dollars but expensive in APR. A $20 fee on a $100 advance repaid in 7 days is a 1,043% APR. Cheap-looking fees are deceptive on short terms.

- Tribal-affiliated lenders claiming sovereign immunity. These lenders argue state APR caps do not apply to them. APRs can hit 700%+.

- Default tips set at 10% to 20%. The FTC's pending complaint against Dave (filed November 2024) alleges this pattern specifically.

- Apps that report only positive payments. Sounds good, is actually a warning sign. A legitimate credit-builder reports positive and negative, because that is what the bureaus require for accurate data.

- Rollovers marketed as "grace periods." Every rollover is another fee. CFPB data shows more than 80% of payday loans are reborrowed within 30 days.

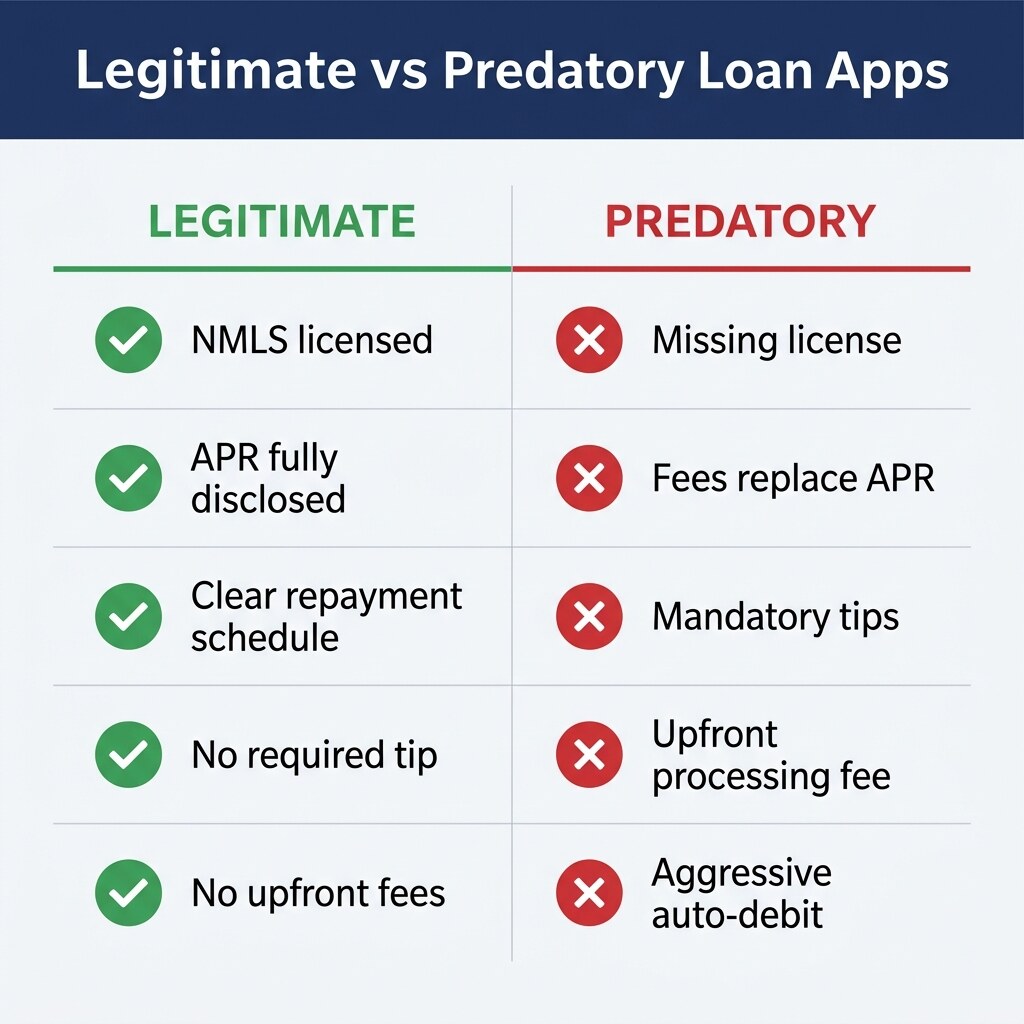

The 7-Point Predatory-vs-Legitimate Scorecard

Before you sign, run the app through this. If it fails 3 or more, walk away.

- Full fee schedule is visible before signup. Subscription, expedite, and tip defaults all on one page.

- Clear $0 tip option. Not buried, not guilt-tripped, not hidden behind "help us keep the lights on" copy.

- APR disclosed, even where state law does not require it. Legitimate lenders lead with the number. Predatory ones hide it.

- State-licensed in your state. Check your state's financial regulator website (it is usually called the Department of Financial Institutions or similar).

- No mandatory arbitration that waives class action without an opt-out. Many legitimate lenders include arbitration but give you 30 to 60 days to opt out. Predatory ones give you no exit.

- On-time payments reported to at least one credit bureau. If the goal is rebuilding, a non-reporting app is a dead end.

- No prepayment penalty. Paying early should save you money, always.

How to Use a Sub-580 App to Rebuild, Not Dig Deeper

If you are sub-580 and you need to borrow, there is a way to do it that improves your situation in six months. There is also a way to do it that leaves you in a worse spot in six weeks. The difference is mostly behavior, not product.

The rebuild path looks like this:

- Borrow once. One loan from a bureau-reporting app (Possible Finance for small amounts, OppLoans for $500+). Not two. Not one from Possible plus one from Dave.

- Make every payment on time. Set up autopay the day the loan funds. Payment history is 35% of your FICO score, the largest single factor.

- Do not reborrow the day you pay it off. Wait at least 30 days. Let the account close out in good standing on your report.

- Layer in a credit-builder account. Self, Kikoff, or MoneyLion Credit Builder Plus. $25 to $35 a month, reporting to all three bureaus, for 12 months.

- Pull your credit report every 60 to 90 days. AnnualCreditReport.com is free every week. Watch the score move.

Six months of that pattern typically moves a sub-580 file into the 580 to 640 range. Twelve months of it often lands in the 640 to 680 range, where mainstream personal loan APRs drop from 30%+ to 15% or lower. That is the exit from the "subprime tax."

When to Say No and Use a Credit Union PAL, a Secured Card, or a CDFI Instead

A loan app is not always the best tool, even when it is the fastest. Two situations where you should probably stop and consider alternatives:

First, if you need less than $2,000 and you have 30 days of flexibility, a Payday Alternative Loan (PAL) from a federal credit union is almost always cheaper. PAL APRs are capped at 28% by federal rule (NCUA). You typically have to be a credit union member for at least one month before qualifying.

Second, if you are trying to rebuild credit rather than pay an emergency bill, a secured credit card beats any loan app. Discover it Secured, Capital One Platinum Secured, or your local credit union's secured card all accept deep subprime applicants, report to all three bureaus, and let you graduate to an unsecured card within 6 to 12 months if you pay on time.

Third, if you are in a community served by a CDFI (Community Development Financial Institution), their small-dollar loan products are often priced at 18% to 24% APR with human underwriting that does not auto-decline on FICO. The CDFI Fund runs a searchable locator at cdfifund.gov.

Servicemembers and their dependents have an additional protection: the Military Lending Act caps most consumer credit at 36% APR. If an app quotes you anything above 36% and you are military, they are probably not allowed to lend to you. Document the quote and report it to the Defense Department's consumer complaint hotline.

State APR Caps Worth Knowing

Your state's cap (the maximum APR a lender can charge on a small-dollar loan) affects which apps can legally operate in your zip code.

- 18 states plus DC cap at 36% APR or ban payday lending outright. If you live in one of these states, most high-APR loan apps either will not lend to you or will structure around the cap in ways worth scrutinizing.

- Illinois and New Mexico capped at 36% APR in 2021 and 2023 respectively.

- New York caps civil usury at 16% APR, criminal usury at 25%.

- Texas, Florida, California, and Georgia have higher or more permissive caps, which is why most app-based subprime lenders concentrate there.

If an app lets you apply from a 36%-cap state and quotes you 160% APR, it is almost certainly structured as a tribal lender, an out-of-state bank partnership, or something operating in a gray area. You can legally accept the loan, but your state attorney general's office may not help if something goes wrong.

The Bottom Line for Sub-580 Borrowers

You have real options. They are not cheap, but they are cheaper than payday storefronts, and some of them actually help you climb out of the tier. Possible Finance and OppLoans are the two apps most likely to get you both the money and the credit rebuild at the same time. Dave, Brigit, MoneyLion, and Earnin can bridge you to payday but will not move your score. SoLo Funds and any tribal-affiliated lender deserve extra scrutiny. A credit union PAL, a secured credit card, or a CDFI loan often beats any of it if you have a few weeks to arrange them.

Borrow once. Pay it off on time. Layer in a credit builder. Pull your report. Six months from now, the options available to you look different.

Common questions from readers.

Short answers to the questions we get by email after this article publishes.

01 Which loan apps approve under a 580 credit score?

OppLoans, Possible Finance, Dave, Brigit, MoneyLion Instacash, and Earnin regularly approve borrowers with FICO scores below 580 because they underwrite on bank-transaction data rather than your credit score. OppLoans and Possible Finance also report on-time payments to the credit bureaus, which means responsible use of these two apps can help rebuild your credit over six to twelve months.

02 Do loan apps do a hard credit check?

Most sub-580-friendly apps do not run a hard credit check. They use a soft pull (which does not affect your score) plus bank-transaction data through Plaid. OppLoans typically pulls an alternative bureau like Clarity. Traditional installment lenders like SoFi, Upstart, and Upgrade do a soft pull when you check your rate and a hard pull only if you accept the loan offer.

03 What is the cheapest loan app for bad credit?

Possible Finance is usually the cheapest app-based installment option for small amounts, charging $10 to $25 per $100 borrowed depending on state, with bureau reporting included. For larger amounts, OppLoans at 160% to 195% APR is cheaper than any storefront payday loan (which averages 391% APR) and is structured as a fixed-payment installment loan with no prepayment penalty.

04 Can I get a personal loan with a 500 credit score?

Yes, from cash-flow-underwritten lenders. OppLoans, Possible Finance, and several online subprime lenders approve applicants with FICO scores around 500 if bank-transaction data shows steady income and manageable spending. Traditional lenders (SoFi, LightStream, Discover) almost always decline at 500. APRs at this credit tier typically range from 100% to 200%, well above prime but below storefront payday loan rates.

05 Will a loan app help me rebuild my credit?

Only if the app reports to the credit bureaus. Possible Finance, OppLoans, Self, Kikoff, MoneyLion Credit Builder Plus, and Brigit Credit Builder report on-time payments to Experian, Equifax, and TransUnion. Pure cash advance apps (Dave, Earnin, Brigit Instant Cash, Chime SpotMe, Klover) do not report to the bureaus, so on-time repayment does not build your credit history or raise your score.