A tip-based loan app charges you interest disguised as a voluntary gratuity, and the real cost is usually an effective APR of 300% to 750% once you add the tip plus any expedite fee to a one-week or two-week payback window. California's Department of Financial Protection and Innovation found that users tip on 73% of transactions that solicit a tip, which is not the behavior of people making a truly free choice. If your last $100 advance came with a $5 tip and a $3.99 expedite fee, you just paid the equivalent of a roughly 470% APR loan.

I want to walk you through the math, the regulatory fight happening right now, and the UI tricks that keep the tip jar full. After 22 years of watching borrowers underestimate short-term credit, I can tell you the tip model is the most expensive thing most people are paying for without realizing it.

Why "optional" isn't really optional

The California DFPI studied this directly and found tip uptake at 73% on transactions where the UI asked for one. Think about that number for a second. Almost three out of four people, every single advance, leave a tip. That is not a rounding-error rate of voluntary behavior. That is a price.

The same DFPI report identified "multiple strategies" apps use to make tipping feel almost as certain as a required fee: pre-selected default amounts, sad-face or smiley-face emoji nudges, framing that implies the tip funds meals for children in need, and the implicit suggestion that tipping affects your future access to advances. None of that is illegal on its face. All of it is engineered.

The math on a real advance

Here is what it actually costs. These are worked examples using typical amounts and payback windows for apps like Earnin, Dave (under its prior tip model), and Cleo.

| Advance | Tip | Expedite fee | Payback window | Effective APR |

|---|---|---|---|---|

| $20 | $2 | $0 | 7 days | ~521% |

| $50 | $3 | $2.99 | 7 days | ~624% |

| $100 | $5 | $3.99 | 7 days | ~468% |

| $100 | $11 | $3.99 | 11 days | ~498% |

| $200 | $10 | $3.99 | 14 days | ~182% |

The 498% number on the $100 advance is not mine. That is the National Consumer Law Center's calculation on an Earnin-style product. A traditional payday loan, the product consumer advocates have been fighting for three decades, runs around 400% APR. Tip-based advance apps are, on average, more expensive than payday lending. They just feel friendlier.

How the UI is designed to trigger tipping

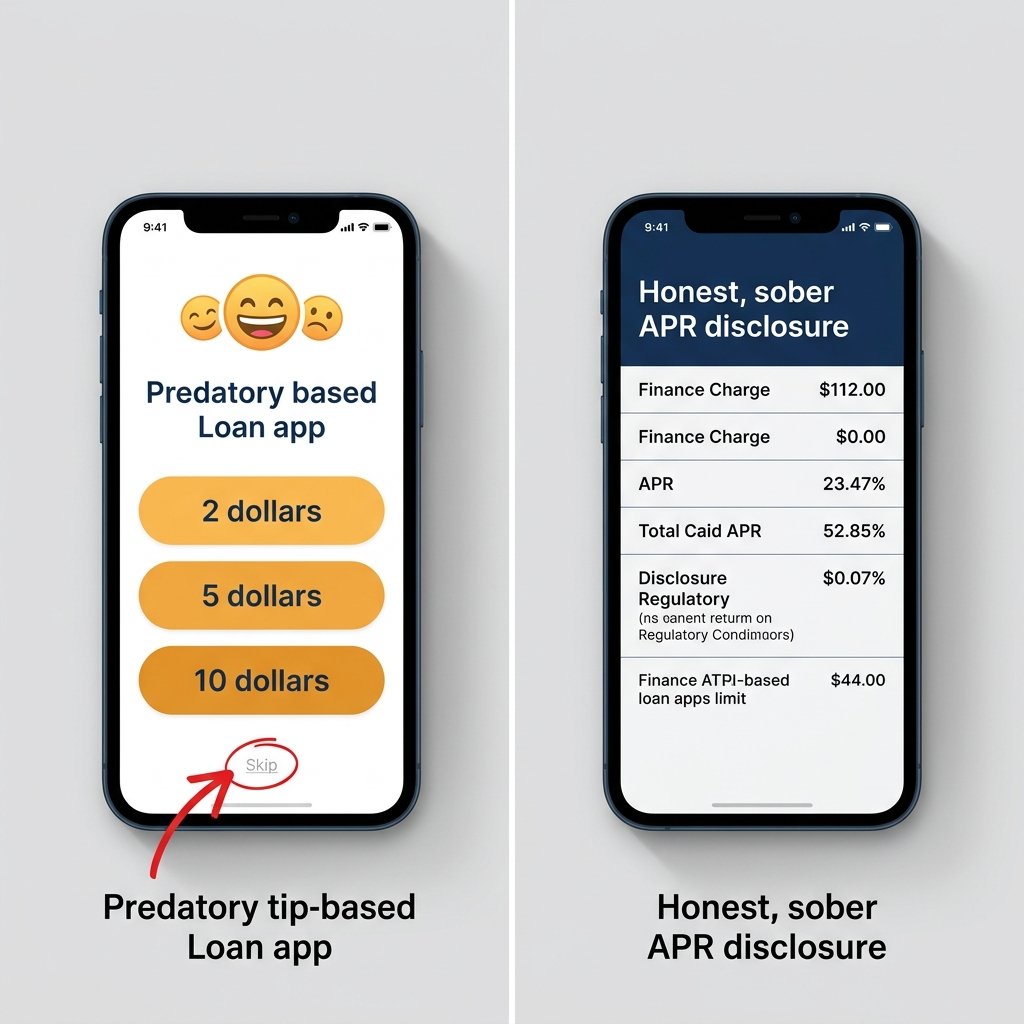

Pull up any tip-based app's advance flow and count the nudges. You will see some combination of:

- A pre-selected tip amount already highlighted when the screen loads.

- Emojis that change expression based on the amount you select. A $0 tip gets a frowning face. A $5 tip gets a smile.

- Copy that implies the tip funds meals for children in need, or supports the community of users.

- A "karma score" or progress bar that appears to tie your tip history to future access to larger advances.

- No clear, equally prominent button for $0.

None of this is accidental. These patterns have names in the UX world. They are called "dark patterns," and the FTC, alongside the CFPB's Junk Fees initiative, has been building enforcement cases around them since 2022.

FTC v. Dave: what the complaint alleges

In November 2024, the Federal Trade Commission filed a complaint against Dave Inc. and its CEO, Jason Wilk. The complaint alleges Dave collected "tips" of 10% to 20% of the advance amount without clear consent, and that the app represented tips as funding meals for children in need while Dave itself kept most of the money. The DOJ amended and joined the complaint in December 2024. The case is still pending as of early 2026.

Dave changed its fee model in February 2025, shifting from tips to a flat 5% fee with a $5 minimum and a $15 cap. Current Dave users no longer see the old tip prompt. That is worth noting clearly: the Dave app today is not the Dave app the FTC sued over. But the underlying question, whether a voluntary-looking payment that 73% of users make is actually voluntary, is very much live.

California and New York: states are not waiting for the federal answer

The California DFPI signed a Memorandum of Understanding with Earnin back in 2021 that permitted "optional" tips under certain disclosure conditions. In 2023, DFPI proposed a rule that reclassifies tips and donations as "charges" subject to California's state fee and interest caps. Under that framing, several apps would be in violation of state usury limits.

New York went further. In April 2025, the NY Attorney General sued MoneyLion and DailyPay, alleging effective rates "frequently up to 750%" once tips and fees are factored in. The suit invokes New York's longstanding civil and criminal usury caps, which sit at 16% and 25% respectively. Those caps exist specifically to prevent the product being sold.

The CFPB's December 2025 pivot

On December 23, 2025, the CFPB issued an Advisory Opinion declaring that tips and expedited-delivery fees are not "finance charges" under the Truth in Lending Act for products that qualify as "covered EWA" (earned wage access). That opinion rescinded the opposite position the CFPB had taken in a July 2024 proposal.

Translation: federally, tips are getting a pass. At the state level, they are getting treated as interest. Both things are true at the same time. If you live in California, New York, Connecticut, or DC, state regulators are likely to keep pressing the point regardless of where the CFPB lands. If you live in Texas, Florida, or most of the Southwest, federal posture is what you have, and right now that posture is friendly to the tip model.

Calculate the effective APR on your last advance

You can do this on a napkin. The formula is:

APR = (total cost / advance amount) x (365 / days until repayment) x 100

Say you took a $100 advance, tipped $5, paid a $3.99 expedite fee, and the app pulled repayment in 7 days. Total cost: $8.99. Advance: $100. Days: 7.

(8.99 / 100) x (365 / 7) x 100 = 468.8% APR

Run that math on your last three advances. If the number surprises you, you are not alone. Most people who have used these apps for a year or more are spending somewhere between $80 and $200 annually on advance fees they never counted as interest.

Apps that don't use the tip model

Not every cash advance app runs on tips. Here are structures that charge differently:

- Flat subscription: Brigit and MoneyLion charge a monthly membership (usually $8.99 to $9.99) that unlocks advances without per-advance fees. Cheaper than tipping only if you use advances often.

- Flat per-advance fee: Dave (post-February 2025) and Current charge a fixed percentage with a cap, no tip prompt.

- Bank-provided advances: Chime SpotMe and Varo Advance are account-linked and don't use tips at all. SpotMe is free up to your limit; Varo Advance charges a flat fee that scales with the amount.

None of these are free. All of them are cheaper than a 400-to-700% APR advance.

The bottom line

Optional is doing a lot of work in the phrase "optional tip." The design of the screen, the emoji faces, the implication of social good, the 73% uptake rate, all of it says the tip is a price that has been repackaged as a gift. If you use these apps, at minimum calculate the real APR before the next advance. You might still decide it's worth it. That is your call. But it should be a call you are making with both eyes open, not one the UI made for you.

Common questions from readers.

Short answers to the questions we get by email after this article publishes.

01 Are tips on cash advance apps legally required to be disclosed as interest?

Federally, no, as of the CFPB's December 2025 Advisory Opinion, which held that tips and expedited-delivery fees are not finance charges under TILA for covered EWA products. At the state level, California and New York treat tips as charges subject to usury limits, and active lawsuits are testing the boundaries. Your state's rules matter more than the federal default right now.

02 What is a reasonable APR for a short-term cash advance?

There is no perfect answer, but most consumer advocates point to the 36% APR cap applied to active-duty military under the Military Lending Act as a useful ceiling. Subscription-based advance apps typically land between 50% and 150% effective APR when you amortize the monthly fee over your usage. Tip-based advances routinely run 300% to 700%, which is worse than traditional payday loans.

03 If I stop tipping, will the app cut off my access?

Officially, no. In practice, apps that use a "karma score" or a tier system may reduce your advance limit or lengthen your funding time if you consistently tip $0. Earnin has historically scaled the maximum advance amount to tip history for some users. You can test this by dropping your tip to $0 for three advances and watching whether your next approved amount shrinks.

04 Did Dave really misuse tips the way the FTC says?

The FTC's complaint alleges Dave collected 10% to 20% tips without clear consent and implied tips funded meals for children while Dave retained most of the money. The case is still pending as of early 2026. Dave changed its fee model to a flat percentage in February 2025, so current Dave users are no longer seeing the tip prompt that the FTC action is centered on.

05 Is there any loan app that's genuinely free?

No. Every cash advance product has a cost somewhere, whether it is a subscription, a percentage fee, an expedite charge, or a tip. The closest thing to free is a bank-provided overdraft buffer like Chime SpotMe, which has no per-use fee up to your limit. Even there, the "free" piece is cross-subsidized by the bank's interchange revenue from your debit-card spending.