A typical US loan app collects seven categories of data about you: identity (name, SSN, driver's license), bank-linked transaction history through Plaid or a similar aggregator, device identifiers, approximate or precise location, credit-header data from the bureaus, behavioral signals like how long you hovered on the SSN field, and third-party enrichment from data brokers. Most of that data leaves the app through advertising and analytics SDKs within the first 90 seconds of your session, and you have real, enforceable rights to cut off that flow in at least seven states, including California, Virginia, Colorado, Connecticut, Utah, Oregon, and Texas.

I'll walk you through exactly what happens after you tap Apply, who ends up with the data, and the 10-minute checklist that actually cuts the pipeline. The goal here isn't paranoia. It's doing the housekeeping the privacy law already says you can do.

What happens in the 90 seconds after you tap "Apply"

The app loads. Before you type a single character, the SDKs embedded in the app have already phoned home. Firebase logs the session open. AppsFlyer or Branch records which ad you came from. Meta Audience Network and Google Ads attach the install to your advertising profile. A fraud-detection SDK like Socure or Persona is already fingerprinting your device: OS version, carrier, IP address, rooted-or-jailbroken status.

You type your name. That triggers another event. You type your SSN. Another event, and in some apps a behavioral flag if you paused or deleted and retyped. You tap the Plaid button to link your bank. Plaid opens in a sandboxed webview, you authenticate to your bank, and Plaid pulls transaction history, balance, recurring income, and overdraft frequency back through its API to the loan app.

By the time you see "Checking your eligibility...," roughly 15 to 25 third parties have received some piece of your session. None of that is illegal in most states. It is, however, disclosed in the privacy policy you scrolled past, and it is stoppable.

Seven data categories loan apps collect

- Identity data. Legal name, date of birth, Social Security number, driver's license scan (front and back), sometimes a selfie for liveness verification. This is the irreversible stuff. Once it's out, it's out.

- Bank-linked data via aggregators. Plaid, Finicity (owned by Mastercard), MX, and Yodlee read transaction history, account balances, direct-deposit patterns, and overdraft frequency from your linked accounts. Plaid alone connects to more than 12,000 financial institutions and is used by thousands of fintech apps.

- Device and technical data. Device ID, advertising ID (IDFA on iOS, AAID on Android), IP address, mobile carrier, OS version, screen resolution, time zone.

- Location data. Approximate (IP-based) or precise (GPS), depending on what permissions you granted. Google Play now bars personal-loan apps from requesting precise location, but approximate location is still standard.

- Credit-header data. Not the full credit report, but the name/address/SSN match information credit bureaus package for identity-verification vendors. Used to match you to existing files.

- Behavioral data. Time spent on each screen, scroll depth, abandonment points, whether you switched to another app mid-session. Highly valuable for segmentation.

- Third-party enrichment. Data the app buys about you from brokers and attaches to your file: employer, income estimate, other financial products you hold, even household composition.

The SDK pipeline: how data leaves the app

Most users think the loan app itself is the only party collecting data. It isn't even close. A typical fintech app bundles 15 to 30 third-party SDKs, each with its own data-sharing contract. The usual suspects:

- Analytics: Firebase, Mixpanel, Amplitude, Segment.

- Advertising and attribution: Meta Audience Network, Google Ads, AppsFlyer, Branch, Adjust.

- Identity and fraud: Socure, Persona, Alloy, Sift.

- Financial aggregation: Plaid, Finicity, MX, Yodlee.

Data flows from the SDK to the vendor. From the vendor, much of it flows to ad networks. Ad networks sell audience segments to data brokers, who sell them back to other lenders and insurers. That is why one loan application often produces twelve text offers from unrelated lenders within a week. The same SMS spam stream fake loan apps ride on, incidentally.

Your rights by state

This is where the pipeline can actually be interrupted. As of 2026, the following states have comprehensive consumer privacy laws you can invoke, and more states come online every year.

| State | Law | Core rights | Enforcer |

|---|---|---|---|

| California | CCPA / CPRA | Know, delete, correct, opt out of sale/share, limit sensitive data | CPPA and AG |

| Virginia | VCDPA | Access, delete, correct, portability, opt out | Attorney General |

| Colorado | CPA | Access, delete, correct, opt out; GPC honored | Attorney General |

| Connecticut | CTDPA | Access, delete, correct, opt out; GPC honored; neural data added July 2026 | Attorney General |

| Utah | UCPA | Access, delete, opt out of sale and targeted ads | AG and Division of Consumer Protection |

| Texas | TDPSA | Access, delete, correct, portability, opt out; GPC honored | Attorney General |

| Oregon | OCPA | Access, delete, correct, portability, opt out | Attorney General |

Heads up on one wrinkle: the Gramm-Leach-Bliley Act (GLBA), a federal financial-privacy law (the CFPB's Section 1033 rule sits next to it), preempts some state rights for "nonpublic personal information" collected inside an active financial-services relationship. That means some core loan-application data is partially shielded from state deletion requests. Marketing data, location data, behavioral data, and third-party enrichment are not shielded and remain fully subject to state law. In practice, most of what you want to delete is the second bucket, not the first.

The 10-minute opt-out checklist

1. Turn on Global Privacy Control

GPC is a browser-level signal that automatically tells websites "do not sell or share my data." Eleven-plus states now require covered businesses to honor it. Turn it on in Firefox (Settings, Privacy & Security, "Tell websites not to sell or share my data"), in Brave, or via the DuckDuckGo browser. Safari and Chrome still require an extension.

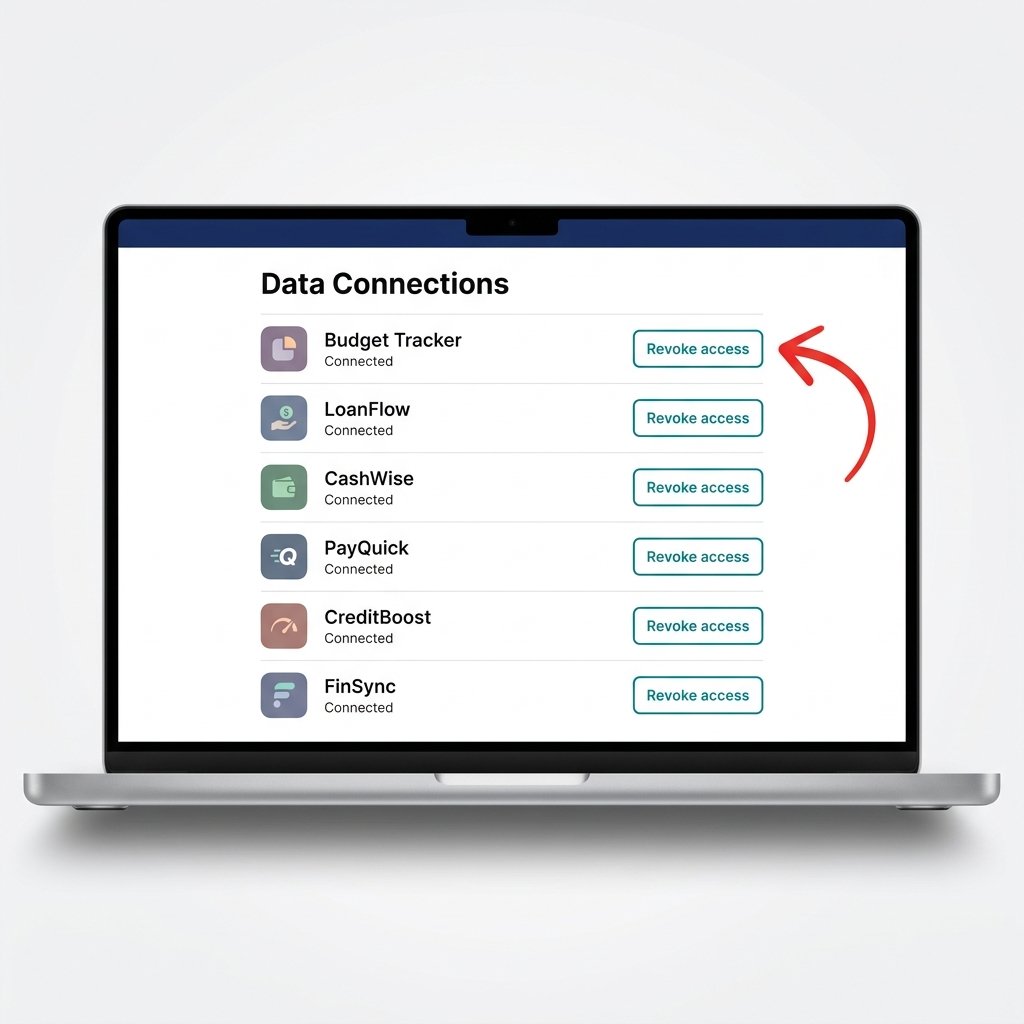

2. Revoke Plaid access at my.plaid.com

Plaid refreshed its consumer portal in 2024. Go to my.plaid.com, authenticate, and you will see every app that has ever connected to your bank through Plaid. You can disconnect and request deletion of your Plaid-side data on a per-app basis, which also tells the aggregator to stop pushing fresh transaction data to that app.

3. File a CCPA or state-law deletion request

Every covered business must provide a way to submit a deletion request. Look for a "Do Not Sell or Share My Personal Information" link in the app or on the company's website, or an email address at privacy@ or dpo@. File the request, reference the state law by name (CCPA, VCDPA, CPA, CTDPA, UCPA, TDPSA, OCPA), and keep a copy of the confirmation. They have 45 days to respond.

4. Use the California Delete Act, if you're a CA resident

SB 362 creates a one-stop deletion request through the California Privacy Protection Agency that propagates to every registered data broker in California. The CPPA portal is rolling out in phases through 2026. Bookmark cppa.ca.gov and check back quarterly until the full deletion-sweep feature is live.

5. Adjust App Tracking Transparency and the Advertising ID

On iOS: Settings, Privacy & Security, Tracking, turn off "Allow Apps to Request to Track." On Android: Settings, Security & privacy, Privacy, Ads, "Delete advertising ID." This does not stop all data collection, but it disables the single persistent identifier most ad-network flows depend on.

6. File complaints if you need leverage

For a loan app that ignores a deletion request: CFPB at consumerfinance.gov/complaint, CPPA at cppa.ca.gov, your state AG's consumer-protection office. Companies respond to regulator inboxes far faster than to yours.

The bottom line

You cannot stop a loan app from collecting data at the moment you apply. That is the price of the product. What you can do is cut off the resale pipeline afterward, which is where most of the damage actually happens. Thirty minutes of housekeeping, done once a year, materially shrinks the amount of your financial data floating around the broker ecosystem. Nobody is going to do it for you.

Favor apps that publish clear privacy labels on their App Store and Google Play listings.

Common questions from readers.

Short answers to the questions we get by email after this article publishes.

01 Can I actually delete my data after a loan is closed?

Partially. Under GLBA, lenders can retain core transaction and identity data for as long as required by banking regulations, typically five to seven years. But marketing data, location data, behavioral data, and third-party broker appends fall outside that shield and are fully deletable under state laws like CCPA, VCDPA, and TDPSA. Submit the request and specify those categories explicitly.

02 Does revoking Plaid access close my loan account?

No. Revoking Plaid only stops the aggregator from sending fresh transaction data to that lender going forward. Your loan account, balance, and repayment schedule are unaffected. You may need to re-link if you later want to change payment methods or qualify for another product from the same lender, but the existing loan continues on its terms.

03 Is Global Privacy Control legally binding in my state?

As of 2026, GPC must be honored as a valid opt-out request in California, Colorado, Connecticut, Delaware, Maryland, Minnesota, Montana, New Jersey, New Hampshire, Oregon, and Texas. Other states treat it as a preference signal but don't mandate compliance. Even where not mandatory, many national companies honor it uniformly because segregating users by state is operationally expensive.

04 What data can a loan app never ask for in the US?

Under Google Play's Personal Loans policy, US loan apps cannot request access to contacts, photos, precise location, external storage, call logs, or SMS. Apple applies similar restrictions through App Review Guideline 1.4.3. If a loan app asks for any of those permissions on install, it is either non-compliant (and at risk of being pulled) or not actually distributed through the official stores.

05 How do I find out which SDKs a specific loan app uses?

Check the iOS App Privacy label on the App Store listing or the Data Safety section on Google Play. Both require developers to disclose data categories collected and shared with third parties. For deeper inspection, tools like Exodus Privacy (exodus-privacy.eu.org) reverse-engineer Android APKs and list embedded trackers. It is imperfect but gives you a sense of the SDK density inside any given app.